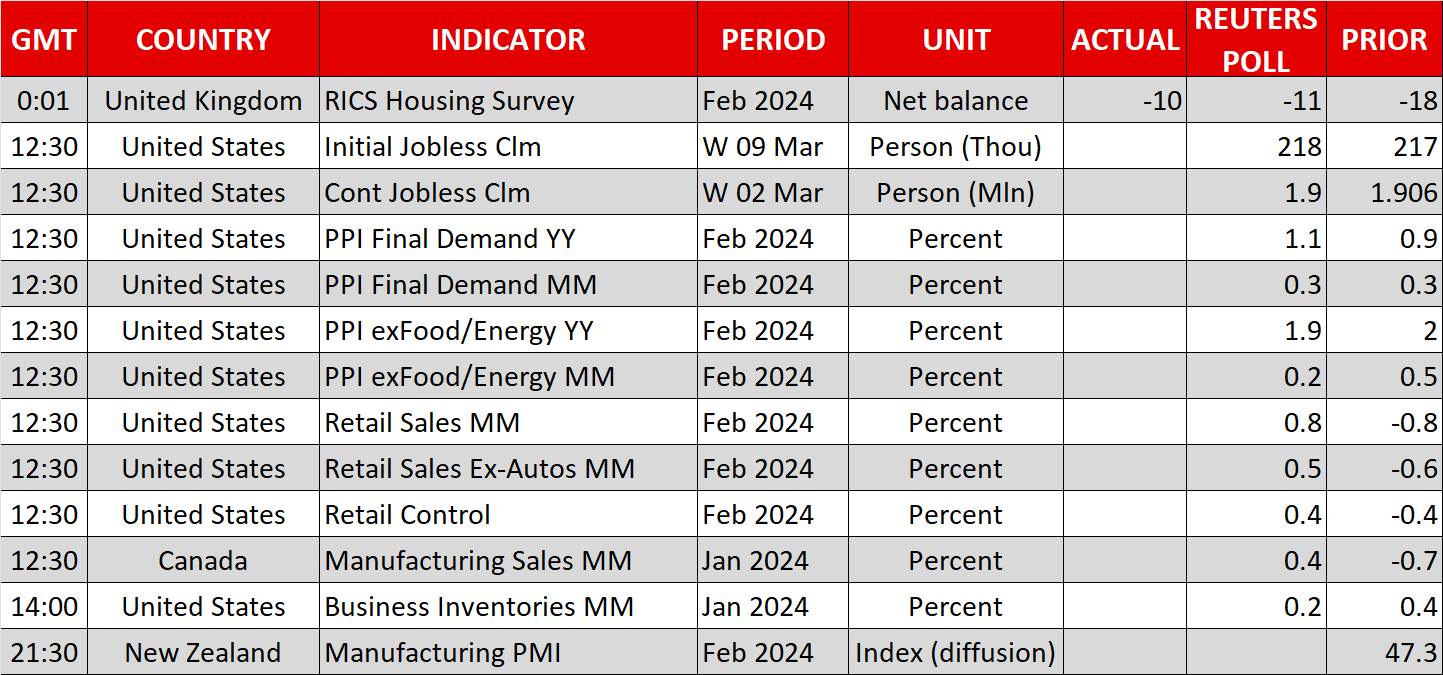

US PPI and retail sales data enter the limelight

NVDA

-3.24%

Add to/Remove from Watchlist

Add to Watchlist

Add Position

Position added successfully to:

Please name your holdings portfolio

Type:

BUY

SELL

Date:

Amount:

Price

Point Value:

Leverage:

1:1

1:10

1:25

1:50

1:100

1:200

1:400

1:500

1:1000

Commission:

Create New Watchlist

Create

Create a new holdings portfolio

Add

Create

+ Add another position

Close

- After hot CPI inflation, dollar awaits PPI and retail sales data

- Yen on the back foot as BoJ March hike bets decrease

- S&P 500 and Nasdaq pull back, gold rebounds

Dollar trades cautiously ahead of US data

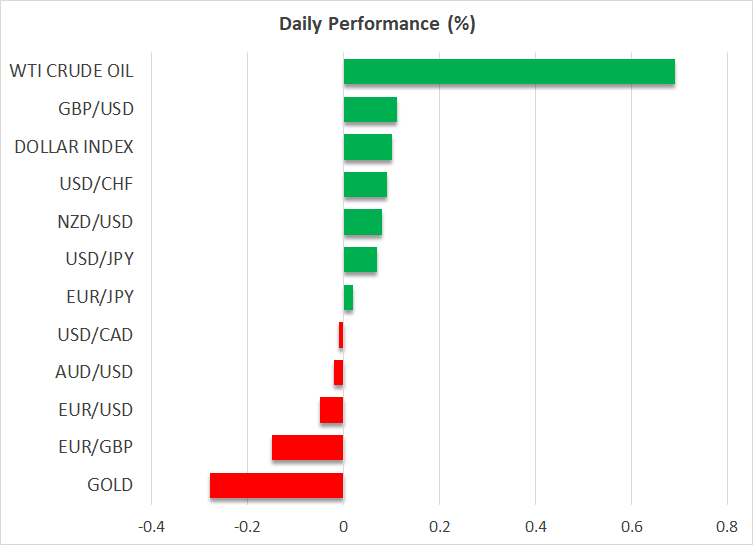

The US dollar traded lower against most of its major peers yesterday, gaining some ground only against the Swiss franc and staying virtually unchanged against the Japanese yen. Today, the greenback is trading slightly higher or unchanged.

It seems that dollar traders have adopted cautious strategies once again, awaiting the US PPI and retail sales data that could shed more light on how the Fed could move forward with monetary policy. On Tuesday, the CPI numbers revealed that inflation was stickier than expected in February, which prompted some market participants to scale back bets regarding a June rate cut.

According to Fed fund futures, from nearly fully pricing in a quarter-point cut in June, investors are now assigning a nearly 75% chance for such a move, with the total number of basis points worth of rate reduction by the end of the year falling to 79, almost matching the Fed’s own projections of 75bps.

If today’s PPI figures corroborate the notion that inflation in the US is proving to be stickier than previously expected and should retail sales rebound notably as the forecasts suggest, then a June cut may become even less likely in the eyes of investors, and thus, the US dollar and Treasury yields may rise somewhat.

However, even if today’s numbers surprise to the upside, the dollar is unlikely to enter a long-lasting uptrend as the market is already in agreement with the Fed. For that to happen, the Fed may need to revise its dot plot higher when it meets next week.

Investors reduce bets for BoJ hike next week

The Japanese yen is on the back foot again today as the probability for the BoJ to exit negative interest rates next week have continued falling to around 40%. Last week, reports that Japanese policymakers may indeed decide to press the hike button as early as at the March gathering added fuel to the yen’s engines, taking the probability for such an action to around 50%. However, on Tuesday, Governor Ueda poured some cold water on such expectations, saying that although the economy is recovering, it is still showing signs of weakness.

All these developments make next week’s decision very important. But ahead of the gathering, traders may pay attention to the initial estimates of the spring wage negotiations on Friday, as the results may prove crucial for the BoJ’s policy assessment. Speculation for another round of strong pay hikes intensified last week after Japan’s largest industrial labor group said that 25 of its member unions have already seen their wage demands being met in full.

Equities retreat, gold rebounds ahead of US data

On Wall Street, the Dow Jones recorded some gains, but both the S&P 500 and the tech-heavy Nasdaq slid as investors took some profits ahead of today’s data and next week’s FOMC decision.

A semiconductors’ index pulled back 2.5%, with shares of Nvidia (NASDAQ:NVDA) easing 1.1%, suggesting that AI-related stocks remain the main driver on Wall Street. Intel’s stock fell 4.4% following reports that the Pentagon had withdrawn a planned $2.5bn chip grant for the company.

Such high-growth tech firms are usually valued by discounting expected cash flows for the quarters and years ahead, and thus, anything suggesting that interest rates are likely to stay elevated for a longer period than currently anticipated may encourage some more selling.

That said, apart from data and events related to interest rates, investors may pay close attention to Nvidia’s global GTC developer conference on AI on March 18-21. Should they stay confident that there are more future growth opportunities to be priced into the market, any interest-rate related retreats are likely to stay limited and short-lived.

Gold rebounded yesterday, boosted by a weaker dollar. If today’s data adds to speculation that the Fed could wait a bit longer before lowering interest rates, the precious metal could pull back. However, such a setback may be treated as a corrective phase as geopolitical tensions are keeping safe-haven demand for the metal intact.