Valuation Metrics, Volatility Suggest Future Market Returns Could Disappoint

US500

+0.51%

Add to/Remove from Watchlist

Add to Watchlist

Add Position

Position added successfully to:

Please name your holdings portfolio

Type:

BUY

SELL

Date:

Amount:

Price

Point Value:

Leverage:

1:1

1:10

1:25

1:50

1:100

1:200

1:400

1:500

1:1000

Commission:

Create New Watchlist

Create

Create a new holdings portfolio

Add

Create

+ Add another position

Close

Valuation metrics have little to do with what the market will do over the next few days or months. However, they are essential to future outcomes and shouldn’t be dismissed during the surge in bullish sentiment.

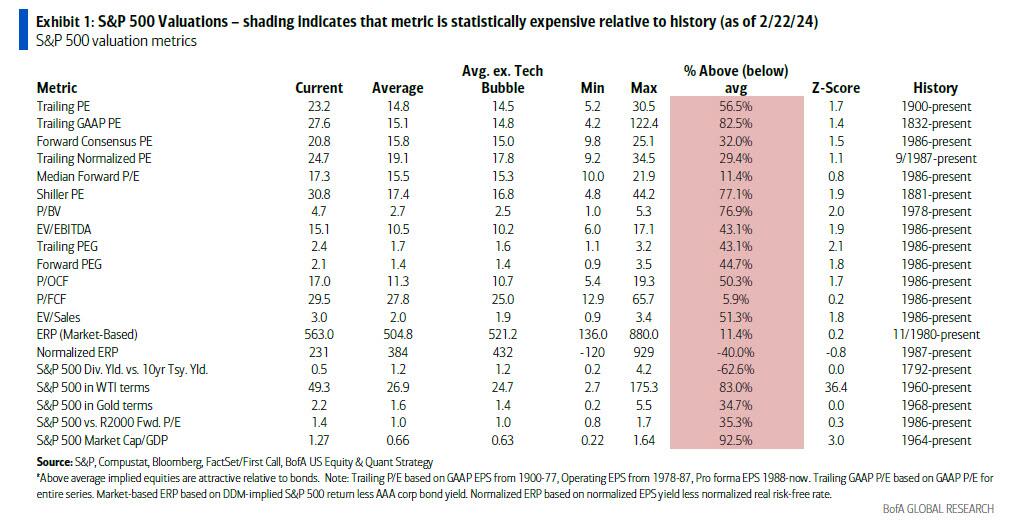

Just recently, Bank of America noted that the market is expensive based on 20 of the 25 valuation metrics they track. As BofA’s Chief Equity Strategist stated:

S&P 500 Valuations

Since 2009, repeated monetary interventions and zero interest rate policies have led many investors to dismiss any measure of Therefore, investors reason the indicator is wrong since there was no immediate correlation.

The problem is that valuation models are not, and were never meant to be, The vast majority of analysts assume that if a measure of valuation reaches some specific level, it means that:

Such is incorrect. Valuation metrics are just that – a measure of current valuation. More importantly, when valuation metrics are excessive, it is a better measure of and the manifestation of the

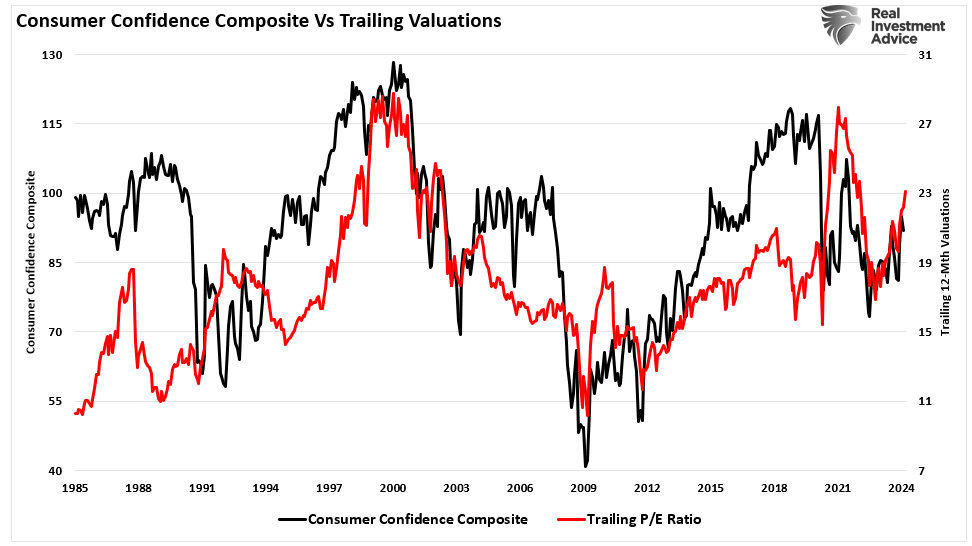

As shown, there is a high correlation between our composite consumer confidence index and trailing 1-year S&P 500 valuations. Consumer-Confidence vs Trailing Valuations

Consumer-Confidence vs Trailing Valuations

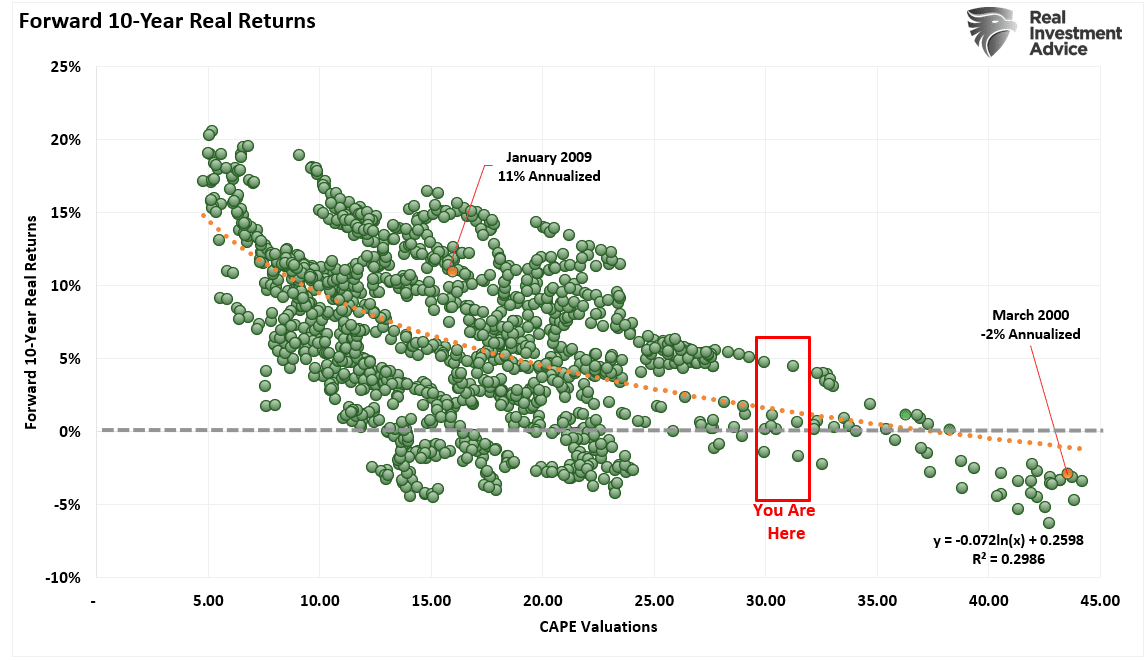

What valuations do provide is a reasonable estimate of long-term investment returns. It is logical that if you overpay for a stream of future cash flows today, your future return will be low.

on this issue in particular:

We can prove that by looking at forward 10-year total returns versus various levels of PE ratios historically. Forward 10-Year Real Returns

Forward 10-Year Real Returns

Asness continues:

Which brings me to Warren Buffett.

Market Cap To GDP

In our most recent newsletter, I discussed with his $160 billion cash pile.

The problem with capital investments is that they take time to generate a profitable return that accretes to the business’s bottom line. The same goes for acquisitions. More importantly, concerning acquisitions, they must both be accretive to the company and reasonably priced. Such is Berkshire’s current dilemma.

This was an essential statement. Here is one of the most intelligent investors in history, suggesting that he cannot deploy Berkshire’s massive cash hoard in meaningful size due to an inability to find acquisition targets that are reasonably priced. With a $160 war chest, there are plenty of companies that Berkshire could either acquire outright, use a stock/cash offering, or acquire a controlling stake in. However, given the rampant increase in stock prices and valuations over the last decade, they are not reasonably priced.

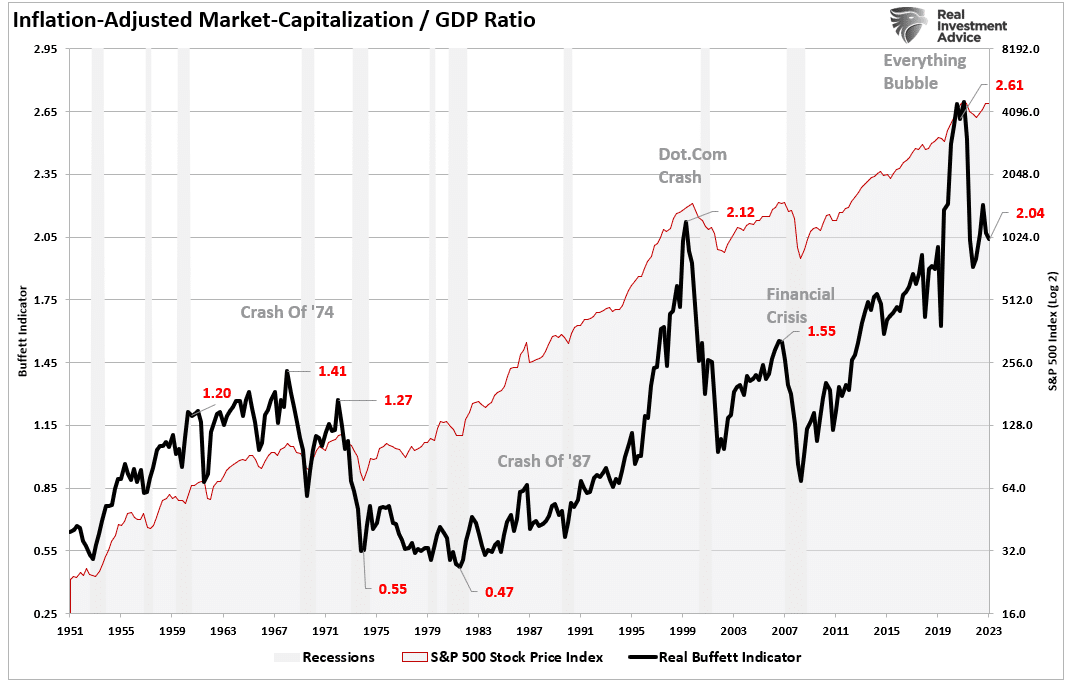

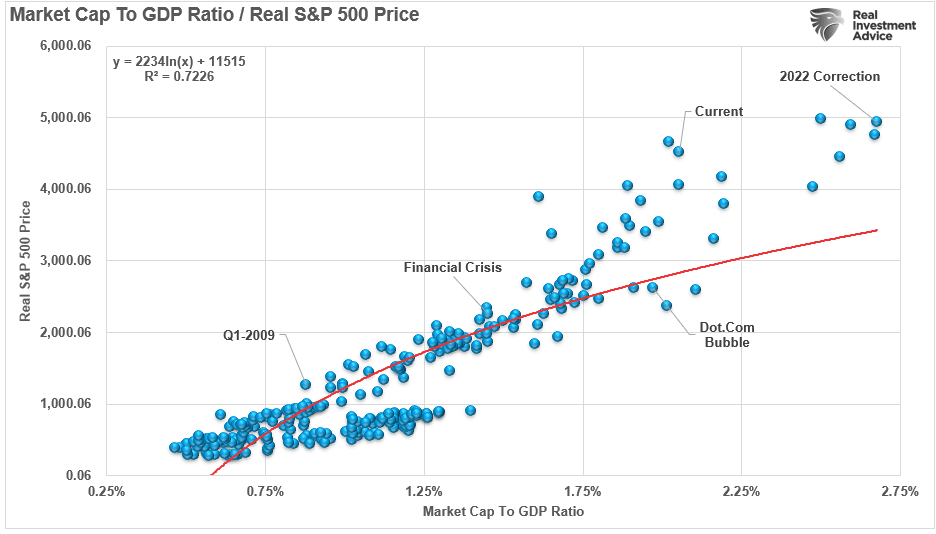

One of Warren Buffett’s favorite valuation measures is the market capitalization to GDP ratio. I have modified it slightly to use inflation-adjusted numbers. The simplicity of this measure is that stocks should not trade above the value of the economy. This is because economic activity provides revenues and earnings to businesses.

Inflation Adjusted Market-Cap To GDP-Ratio

Inflation Adjusted Market-Cap To GDP-Ratio

The confirms Mr. Asness’ point. The chart below uses the S&P 500 market capitalization versus GDP and is calculated on quarterly data. Market-Cap To GDP vs Real S&P 500 Price Chart

Market-Cap To GDP vs Real S&P 500 Price Chart

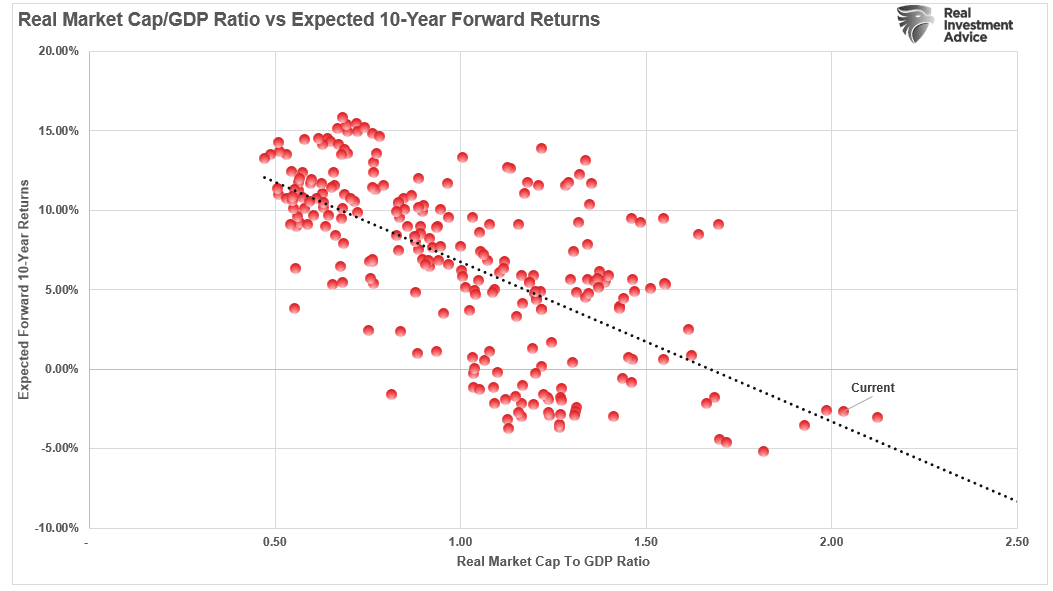

Not surprisingly, like every other valuation measure, forward return expectations are substantially lower over the next ten years than in the past. Real Market-Cap-To-GDP Ratio Vs 10-Year Fwd Returns

Real Market-Cap-To-GDP Ratio Vs 10-Year Fwd Returns

None of this should be surprising. Logics suggests that overpaying for any asset in the present inherently will generate lower future expected returns versus buying assets at a discount. Or, as Warren Buffett stated:

F.O.M.O. Trumps Fundamentals

In the fundamentals don’t matter. In a market where momentum drives participants due to the fundamentals are displaced by emotional biases. Such is the nature of market cycles and one of the primary ingredients necessary to create the proper environment for an eventual reversion.

Notice, I said eventually.

As David Einhorn once stated:

Furthermore, as James Montier previously stated:

As BofA noted in its analysis, stocks are far from cheap. Based on Buffett’s preferred valuation model and historical data, return expectations for the next ten years are as likely to be close to zero or negative. Such was the case for ten years following the late ’90s.

Investors would do well to remember the words of the then-chairman of the SEC, Arthur Levitt. In a 1998 speech entitled ” he stated:

Regardless, there is a straightforward truth.

The economy is slowing down following the pandemic-related spending spree. It is also doubtful the Government can continue spending at the same clip over the next decade as it did in the last.

While current valuations are expensive, it does NOT mean the markets will crash tomorrow, next quarter, or even next year.

However, there is a more than reasonable expectation of disappointment in future market returns.

That is probably something investors need to come to grips with sooner rather than later.