Will Powell Signal Hawkish Shift at Tomorrow’s Meeting?

US2YT=X

-0.76%

Add to/Remove from Watchlist

Add to Watchlist

Add Position

Position added successfully to:

Please name your holdings portfolio

Type:

BUY

SELL

Date:

Amount:

Price

Point Value:

Leverage:

1:1

1:10

1:25

1:50

1:100

1:200

1:400

1:500

1:1000

Commission:

Create New Watchlist

Create

Create a new holdings portfolio

Add

Create

+ Add another position

Close

Analysts are debating if last week’s sticky inflation news is the death knell for a June cut in interest rates by the Federal Reserve. This much is clear: the recent run of news isn’t encouraging for anticipating that a dovish turn for monetary policy is imminent.

On Thursday the government reported that producer price inflation was hotter than expected. Two days earlier, the Bureau of Labor Statistics advised that the Consumer Price Index rose more than expected.

The one-two punch of these reports has further dented confidence that the Fed will soon start cutting interest rates.

There are signs that the US economic growth is slowing, but not enough to trigger concern that the Fed needs to cut rates to counteract the threat of rising recession risk, which remains low at the moment.

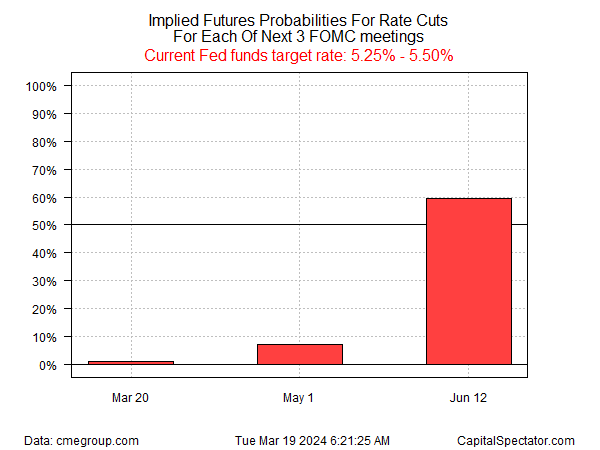

Using Fed funds futures as a proxy for market sentiment indicates a roughly 60% probability that the central bank cuts at its June 12 meeting. That’s down from 70% two weeks ago. Fed Fund Futures

Fed Fund Futures

Looking to the July FOMC meeting, the probability of a rate cut rises by 77%, but a growing number of analysts are skeptical about the timing and, in some cases, the likelihood for a rate cut in 2024.

“The Federal Reserve should not be in a race to cut rates,” says Joseph Davis, Vanguard’s global chief economist.

He tells The New York Times that the economy has been stronger than expected so cutting too soon may allow inflation to run hotter than the Fed wants in 2025. “We have a growing probability that they don’t cut rates at all this year.”

Jim Bianco of Bianco Research agrees:

“I’m in the camp that the Fed does not change policy in the summer of an election year,” he predicts via CNBC.

If they don’t pull the trigger by June, then it’s November [or] December at the earliest — only if the data warrants it. And, right now, the data isn’t warranting it.”

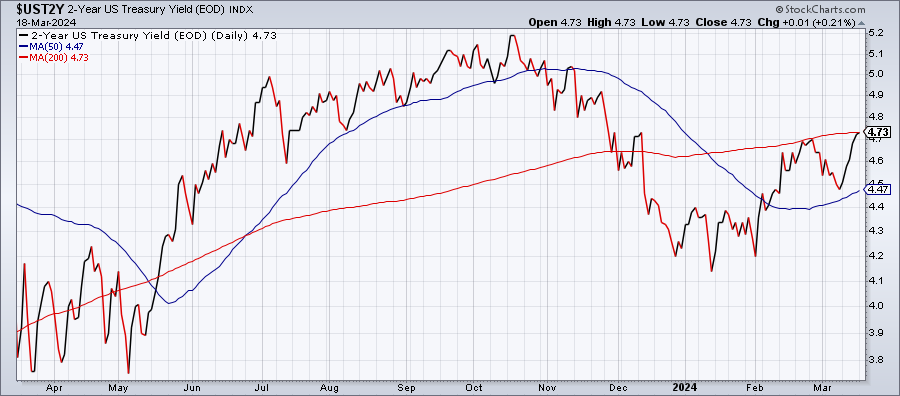

The US Treasury market has been leaning toward that view lately. Notably, the policy-sensitive 2-year yield closed at 4.73% yesterday (Mar. 18), the highest since December.

As a result, this key rate has taken back all of 2024’s decline, which was fueled by rate-cut expectations that have increasingly been thrown into doubt as the year unfolded.

UST2Y-Daily Chart

UST2Y-Daily Chart

Although the Fed is widely expected to leave rates unchanged at tomorrow’s FOMC meeting (Mar. 20), investors will be keenly poring over the policy statement, new economic projections, and chairman Powell’s press conference for a fresh round of clues.

“The Fed will keep their forward guidance unchanged while stressing that they need further evidence that inflation is on a sustainable path toward their 2% target before cutting interest rates,” predicts Ryan Sweet, chief U.S. economist with Oxford Economics, in a research note on Monday.